In an industrial society, sales costs were negligible. Sales was easy to perform when demand was ever-increasing and focus was on how to produce as efficient as possible to meet demand. Now, the paradigm shift is happening with full power where customer is the new king, leading to exploding competition and harder to sell. Not only new competitors through globalization have seen the daylight, but also new methods like e-commerce gain market share at the expense of human based sales forces.

For those organizations that stick with their sales force, sales costs are peaking. The problem is that they just don’t know how to attack them. To decrease cost, companies use the first weapon they see – to fire sales reps. That’s because salary is the only clear choice there are. But at the same time they do, revenues decrease as well.

My standpoint is, firing healthy sales reps is a totally wrong action. Why?

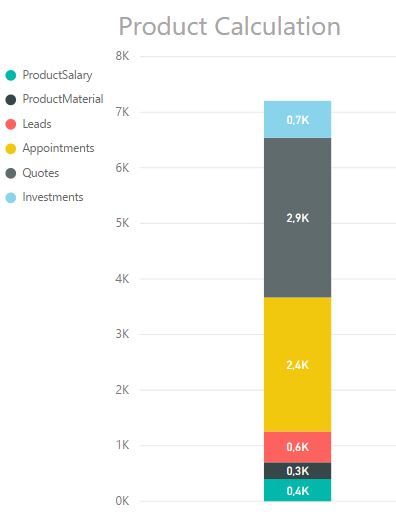

Because the cost of sales salary is minor compared to sales overhead costs. Before, in an industrial society, a product calculation consisted almost only of costs that directly could be connected to a specific product, such as salary for workshop workers and material needed for producing the product. All overhead costs, like the cost for sales, were very small compared with production salaries and direct material costs.

Now, in a post-industrial society, the situation is the reverse. Overhead costs, such as sales costs, are in many cases dominating the product calculation. Many products have over 80% defined just as “overhead costs”.

So, firing a sales rep for the reason of cost is not an efficient way to improve your sales department. To decrease your sales costs, you need to get into those “sales overhead costs” to really understand how to improve.

The challenge is that these overhead sales costs are hidden by a “cost fog” with no or very little transparency. But it shouldn’t be that way. I’m involved in the expertscenario initiative which propose a solution to remove the overhead fog and providing a way for your organization to implement continuous improvements and, finally, be able to attack the massive overhead costs.

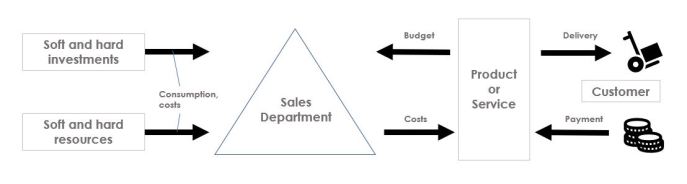

The initiative, with methods like Post-Industrial Accounting Models and Management Models can be applied to all areas in your company, as well as value chain. Overhead sales costs are just one example. To make this example as clear as possible, the initiative has created an app where you may put in your sales plan – such as target revenue, average order size, no of sales reps, hitrate etc – and simulate your sales costs by the process stages Lead, Appointment and Quote, to fulfill your plan. You may also get into the details for each of the stages, to see how sales costs are distributed on different sales tasks, like meeting time, travel time, quote creation, segment prospect database, sales review etc. Very useful to start changing how to work with things in your sales process.

A certain sales plan gives specified costs not only per process stage, but also updates your product calculation, so are able to see how profitable (or not) your current products are, with sales overhead costs taken into account.

The app is not yet launched, but you may get a great feeling how it will be working in a preview.

The app, as well as the models the expertscenario initiative provides, removes uncertainties about what costs that truly affect achievement of your sales plan. In the same perspective, you cannot overlook investments you do within your sales organization either. It may be investments in “soft” refinement such as strategy, process, human resources, CRM etc. Today, most of these investments are accounted upfront – the entire investment the first year – as an overhead lump sum. Instead, the right thing to do would be to spread the investment on several years the investment contribute to the value for the sales organization.

A clear picture of what sales costs you really have is still covered by the overhead fog. Why this is done, I don’t really know, but one clue is the fact that people sometimes don’t like to be measured too much. Better then, thinks leaders, to just spray those costs over entire organization than actually get the picture of what’s working and what’s not.

Believe it or not. It’s soon 2018…and still we are hiding from the scary truth…

The good news is that all I’ve written above is within the framework of GAAP (Generally Accepted Accounting Principles) and the models were already featured in The Hidden Treasure Chests (1993), written by Bert-Olov Bergstrand and Christer Lundgren. The Hidden Treasure Chest has the Swedish Association of Graduates in Business Administration and Economics signature.